8. Mundell-Fleming Model with a

Floating Exchange Rate

(No handout; chapter 13)

What is the Mundell-Fleming model?

In an open economy with external trade and financial transactions, how are

the key macro variables (GDP, inflation, balance of payments, exchange rates,

interest rates, etc) determined and interact with each other? What are the effects of fiscal

and monetary policies? The Mundell-Fleming model is the standard open

macroeconomic model that tries to answer these questions. Most open macroeconomy

models in the textbooks are variations of the Mundell-Fleming model.

Theoretically, it is the most popular model. But its

applicability to actual policy making is not as high as we would hope

(especially for developing and transition countries). Blind

application of this model to your country may not yield good results,

because the model is based on many assumptions which may be unrealistic. But this is the best model that economists have. So use it

carefully.

In

1963 when he was young, Prof.

Robert Mundell (photo) was working with Marcus Fleming at the IMF and

wrote a paper which gave birth to this model. He has been at Columbia University

(New York) in the last 25 years. He has been a strong advocate of stabilization of

major currencies and establishment of euro. In 1999, he won the Nobel Prize

in economics, partly because of the Mundell-Fleming model.

In

1963 when he was young, Prof.

Robert Mundell (photo) was working with Marcus Fleming at the IMF and

wrote a paper which gave birth to this model. He has been at Columbia University

(New York) in the last 25 years. He has been a strong advocate of stabilization of

major currencies and establishment of euro. In 1999, he won the Nobel Prize

in economics, partly because of the Mundell-Fleming model.

The Mundell-Fleming model is an open macro application of the standard

IS-LM analysis. More precisely, it is an IS-LM analysis with trade and

international capital mobility. (If you do not know what the IS-LM model is,

you have a problem. Please look at any intermediate macroeconomic textbook

or ask your friend).

Consider the following three aspects of the macroeconomy:

(1) Aggregate demand (IS and LM curves, representing goods and money

markets)

(2) Aggregate supply (production function and labor market)

(3) Balance of payments (current account and capital account)

The usual textbook exposition (with no trade or capital mobility)

combines (1) and (2), with a

downward sloping AD (aggregate demand) curve and an upward-sloping AS (aggregate supply) curve.

The Mundell-Fleming model combines (1) and (3), namely AD and B (balance

of payments) curves. This means that the Mundell-Fleming model (in its simplest version) has no supply side constraint. As in the most

elementary

Keynesian model, it implicitly assumes that capital and labor are generally

underemployed so that any demand stimulus will expand real GDP (rather than

cause inflation).

Let us now look at the construction of the AD curve and B curve below. (I

will basically use the notation of Rivera-Batiz' book but may add a few more

symbols).

Aggregate demand - IS curve

Aggregate demand is composed of two parts: absorption (A, namely, domestic

demand) and trade balance (T, namely, foreign demand). We ignore service trade,

factor income and transfers, so the current account is the same as the trade

balance.

Y = A +

T

(GDP by expenditure decomposition)

where

A = C + I + G (definition

of absorption)

= A (Y, i; G)

A1

>0, A2 <0, A3 >0; G is

an exogenous spending (shift parameter)

[A1 means partial derivative of A with respect to first variable,

etc]

and

T = M* - qM

(definition of trade balance, measured in domestic currency)

= T (q, Y*,

Y) T1 >0, T2

>0, T3 <0; foreign income Y* is

assumed fixed

(Y: income C: private consumption I: private investment

G: government spending M: imports M*: foreign imports (=our

exports), i: interest rate)

Note that A and T are defined as real variables (deflated by

domestic price P). The real exchange rate q is defined thus:

q = EP*/P

(a rise in q means real depreciation of home currency)

Please note that T1 >0, namely, partial derivative of trade balance

with respect to q is positive. This means that the Marshall-Lerner

condition is satisfied, so real depreciation will improve the trade balance

(when other variables remain unchanged).

From above, we have

Y = A (Y, i; G) + T (q, Y*,

Y)

= F (Y, i, q;

G)

Note: 0 < F1 < 1 [can you explain why?]

Collecting Y to the left-hand side,

Y = f (i, q; G)

f1

<0, f2 >0, f3 >0

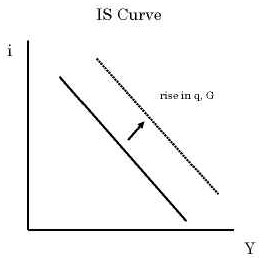

This is our IS curve. It is downward-sloping in the (i, Y) plane. Moreover, a

rise in q (real depreciation) or a rise in G (government spending) shifts the IS

curve up and to the right.

Aggregate demand - LM curve

The LM curve is the same as in the domestic macro version. It shows the

condition for money market equilibrium.

In particular, we ignore the possibility of "currency

substitution," a phenomenon where domestic citizens hold foreign

currency (typically US dollar) as well as domestic currency, and change

their relative shares as circumstances change. No currency substitution is a reasonable

assumption in developed countries, where people hold only domestic currency.

But in many developing countries, currency substitution may be a big factor

that influences the money demand.

Currency substitution is also called

"dollarization." But dollarization has two meanings: (1) the

situation where people use dollars in addition to domestic currency,

because they do not trust the latter (in this case, the monetary authority

usually tries to prevent the use of dollar); (2) the situation where the

government declares that the national currency is the US dollar, abolishes the

central bank, and gives up independent monetary policy. Currency

substitution is equivalent to the first (traditional) meaning of dollarization.

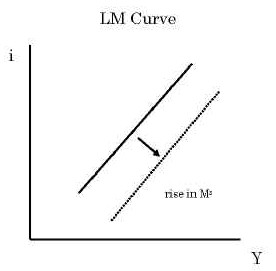

The LM curve is simply:

Ms/P = LD (i,

Y) LD1

<0, LD2 >0

(Ms: money supply P: price level)

As in the domestic version, it is upward-sloping in the (i, Y) plane. A

rise in money supply Ms shifts the LM curve down and to the

right. In this formulation, the price level P is assumed fixed. This may be

unrealistic in a small open economy where exchange rate pass-through (E

-> P) is significant.

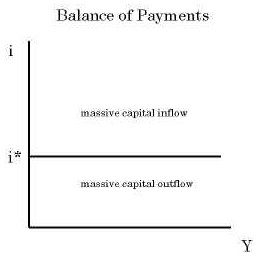

Balance of payments

The balance of payments (B) is the sum of current account (T) and capital

account (K). Remember, for simplicity we have assumed away the flows of

service, factor income and transfers so that the current account is

identical with the trade balance.

B = T + K

= T (q, Y) + K (i - i*)

T1 >0, T2 <0; K1

> 0

= 0

Here, we assume the following:

--The exchange rate is floating (the real exchange rate q is also

flexible).

--The monetary authority does not intervene in the foreign exchange

market. This means that there is no change in international reserves,

the monetary account is zero, and therefore the current account and the

capital account must always add up to zero (T + K = 0).

--Additionally, we assume perfect capital mobility. This means

that i = i*, K1 = +∞, and K is indeterminate. In other words, if i > i* there

will be a massive capital inflow into the home country and if i < i*

there will be a massive outflow, so the only way K can remain

finite is when i = i*. When that happens, K can take

any value (positive or negative) to offset T, so that T + K = 0 holds.

--The exchange rate expectation is static. That is to say,

people expect that the future exchange rate will be the same as today's (even

though the exchange rate is floating). This is a simplifying assumption.

Thus, instead of the usual uncovered interest parity (i = i* + x, see lecture

4), we have i = i* (because x = 0).

If we depict this situation in the (i, Y) plane, we have a horizontal

line at i*. The domestic interest rate must be equal to the world interest

rate. There will be a massive capital inflow above that line, and a

massive capital outflow below that line.

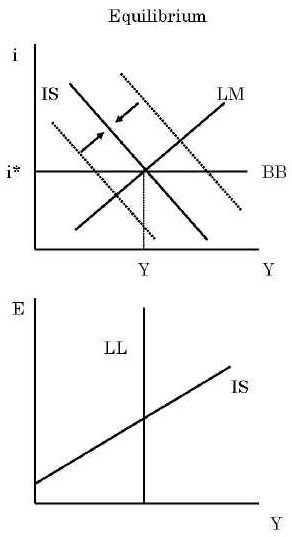

Equilibrium

Under a freely floating exchange rate and perfect capital mobility, the

following three equations derived above determine the equilibrium position.

Y = f (i, q; G)

f1

<0, f2 >0, f3

>0

<IS>

Ms/P = LD (i,

Y) LD1

<0, LD2

>0 <LM>

i = i*

<BOP>

Recall that foreign income, foreign interest rate and domestic price are

all fixed (Y*, i*,

P).

The equilibrium can be pictured as follows:

Comparative statics

Comparative statics means checking how the equilibrium changes if

one input variable is changed. More technically, it is a matrix of signs (+

or -) indicating the changes in endogenous variables in response to a

change in each exogenous variable.

In this model, we ask two specific questions:

(1) Can we increase Y by an expansionary fiscal policy (an increase in G)?

(2) Can we increase Y by an expansionary monetary policy (an increase in Ms)?

G and Ms are the input variables and Y is the output variable

in question. (We may add that these questions themselves reflect the rather

old-fashioned mentality of macroeconomic fine-tuning. More recently, fiscal

and monetary policies are not considered as tools for adjusting real GDP.)

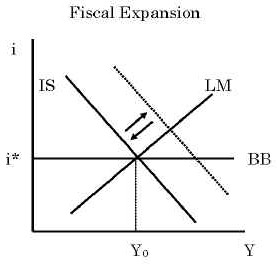

First, consider fiscal expansion.

1. An increase in G shifts the IS curve upward and to the right.

2. This puts an upward pressure on the domestic interest rate (i > i*).

3. But this immediately invites a massive capital inflow.

4. This appreciates the nominal exchange rate E as well as the real

exchange rate q.

5. This worsens the trade balance T.

As the model is constructed, no gradual adjustment is allowed; these events

are supposed to take place instantaneously. The exchange rate appreciates

and the trade balance worsens until the initial increase in G is completely

offset. The IS curve is pushed back to the original position, and Y cannot

increase at all.

What happened is that, in Y = A + T, as A is increased by fiscal

spending, T is reduced by exactly the same amount. Y is unchanged, and only

the relative composition of Y is changed. The conclusion is that under a floating

exchange rate and perfect capital mobility, fiscal policy is ineffective.

Here, "ineffective" means unable to increase Y.

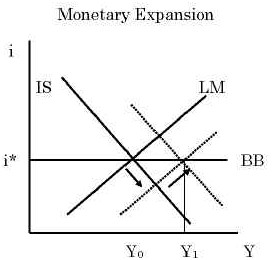

Second, consider monetary expansion.

1. An increase in Ms shifts the LM curve downward and to the

right.

2. This puts a downward pressure on the domestic interest rate (i < i*).

3. But this immediately invites a massive capital outflow.

4. This depreciates the nominal exchange rate E as well as the real

exchange rate q.

5. This improves the trade balance T.

Again, the whole sequence is assumed to take place in an instant.

Compared with the domestic version of IS-LM, monetary policy is more

powerful because the outward shift of LM invites an additional outward shift

of IS. Both LM and IS cooperate to increase income. The conclusion is that under a floating exchange rate and perfect capital

mobility, monetary policy is very effective.

These conclusions are significantly different from those of the domestic version of

the IS-LM model. In the domestic version, fiscal and

monetary policies are both effective, and their relative effectiveness depends

on various elasticities and slopes. But in this case, one policy is utterly

impotent and the other policy is doubly potent. By now, you should clearly

see why (by what mechanism and assumptions) these conclusions are generated.

In the next lecture, we will examine the case where the exchange rate is

fixed. You will see that conclusions on the two policies are completely

reversed. The Mundell-Fleming model produces extreme results.

Once again, let us summarize the Mundell-Fleming assumptions:

--Free float [this assumption can be changed--see next lecture]

--Perfect capital mobility [this assumption can also be modified]

--There are under-utilized resources and there is no supply constraint

--The Marshall-Lerner condition is satisfied

--The price level is fixed (in particular, there is no exchange rate

pass-through)

--No dollarization (no currency substitution)

--Exchange rate expectation is static and/or there is no risk premium

--Foreign P*, Y*, i* are given

Make sure all (or almost all) of these assumptions are met

before applying this model to the real world.

The Dutch disease

[See pp.355-357 in the Rivera-Batiz book]

As an appendix to the Mundell-Fleming model, we would like to discuss the

Dutch disease. This is an important question for many developing and

transition countries, especially those which have a lot of natural resources,

or receive a large amount of ODA, FDI or remittances relative to GDP.

Question: are countries with rich natural resources (oil, minerals,

etc) more likely to industrialize?

It may seem that having a large amount of natural resources is a big advantage for

industrialization because the nation can earn more foreign currency for investment.

But history shows that this is not necessarily so. Japan, Korea, Taiwan,

Singapore, Hong Kong and other countries that succeeded in catching up have

relatively high population density and relatively few natural resources. On the

other hand, Saudi Arabia, Kuwait, Brunei, Bolivia, Nigeria and other countries richly

endowed with natural resources have not industrialized.

Some economists (Jeffrey Sachs, for example) even argue that having no natural

resources is better for industrialization. Perhaps it is human resources,

not natural resources, that count.

But why so? The Dutch disease hypothesis provides one possible

explanation.

In the 1960s, with fixed exchange rates under the Bretton Woods system,

the Netherlands discovered off-shore natural gas. As natural gas was

extracted, it increased domestic income and spending. Investment was

redirected toward the natural gas sector. Dutch wages and prices

began to rise gradually. The Dutch guilder became overvalued in real terms,

their industrial products became uncompetitive, and the manufacturing sector shrunk.

This phenomenon of de-industrialization in the presence of rich natural resources was called the Dutch disease. They

got natural gas but lost manufacturing.

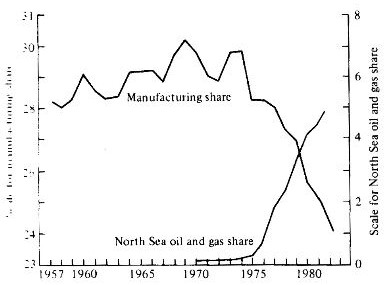

In the late 1970s and early 80s, the UK experienced similar

de-industrialization under a floating exchange rate regime. They discovered

and exploited the North Sea oil fields. Since the global oil price was rising, the UK was expected to earn a great amount of foreign exchange in the

future. But even before these earnings were realized, the British pound

appreciated suddenly in both nominal and real terms. This damaged the

British manufacturing sector.

UK Experiences De-industrialization as Oil Production

Begins

Source: F.L & L.A. Rivera-Batiz, International

Finance and Open Economy Macroeconomics (Optional Textbook), 2nd ed.,

1994, p.357. The left scale for manufacturing share and the right scale for

oil & gas share in GDP.

Definition; the Dutch disease is a situation where an expansion of the

natural resource sector leads to the shrinkage of other tradable industries

through overvaluation.

How overvaluation is generated depends on the exchange rate

regime. Under a fixed exchange rate, overvaluation occurs gradually

through rising domestic wages and prices. Under a floating exchange rate, overvaluation

is more abruptly caused by nominal exchange rate appreciation (often with

overshooting).

The Dutch disease is caused by a large injection of new purchasing power

into the economy. It occurs because domestic factors of production (labor,

capital) are limited while a new discovery creates an additional demand for

these factors. So some existing industries must shrink to make way. The Dutch

disease is most often associated with oil, gas and other minerals, because

they tend to be discovered suddenly and in large amounts. In theory, other

natural resource-based industries such as agriculture, forestry and fishery can also cause

the Dutch disease, but their output changes are usually not as dramatic as mineral

resources.

Moreover, a Dutch disease-like situation (overvaluation) can be generated with large

receipts of ODA, FDI or other capital inflows. If you receive too much

foreign exchange, the exchange rate may stay too high even though domestic

products are expensive and uncompetitive.

Does this mean that having natural resources is a bad thing? Not

necessarily. Natural resources do serve as a shock absorber and a precious

earner of foreign exchange (provided that these earnings are wisely spent). But countries

with a lot of natural resources must conduct economic policies in a

different way than other countries. For example:

--If you rely heavily on a small number of natural resources, you are more

likely to be hit by global price and demand volatility. You should try to

diversify the export base.

--You should also save extra earnings for the rainy day. A special fund

for this purpose is useful. Extra earnings should be saved when the

price is high, and this saving should be used for investment when the price

is low (smoothed spending). Do not invest too much and spend all

earnings when the price is high.

--Use fiscal, monetary and exchange rate policies wisely to soften the

negative shocks to the manufacturing sector, so it does not have to shrink.

--Build a mechanism where natural resource revenues are directed toward

productive investment. Make sure the money is not siphoned off

politically.

--Have a comprehensive and long-term development plan, while

preparing for possible shocks. Know how to respond to them.

--Consider well whether the resources should be exported in raw form, or

they should be processed domestically to add value. One of the key

issues is whether domestic processing is internationally competitive in

terms of cost. If domestic processing is cost effective, its development

will promote employment and industrialization. But don't invest in it if the

cost is high; you will waste a large amount of national income.

<References>

Corden, Max, "Booming Sector and Dutch Disease Economics,"Oxford

Economic Papers 36, 1984, pp. 359-380.

Fleming, J.M., "Domestic Financial Policies under Fixed

and under Floating Exchange Rates," IMF Staff Papers, November

1962.

Mundel, Robert, "Capital Mobility and Stabilization Policy under Fixed

and Flexible Exchange Rates," Canadian Journal of Economics and

Political Science, November 1963.